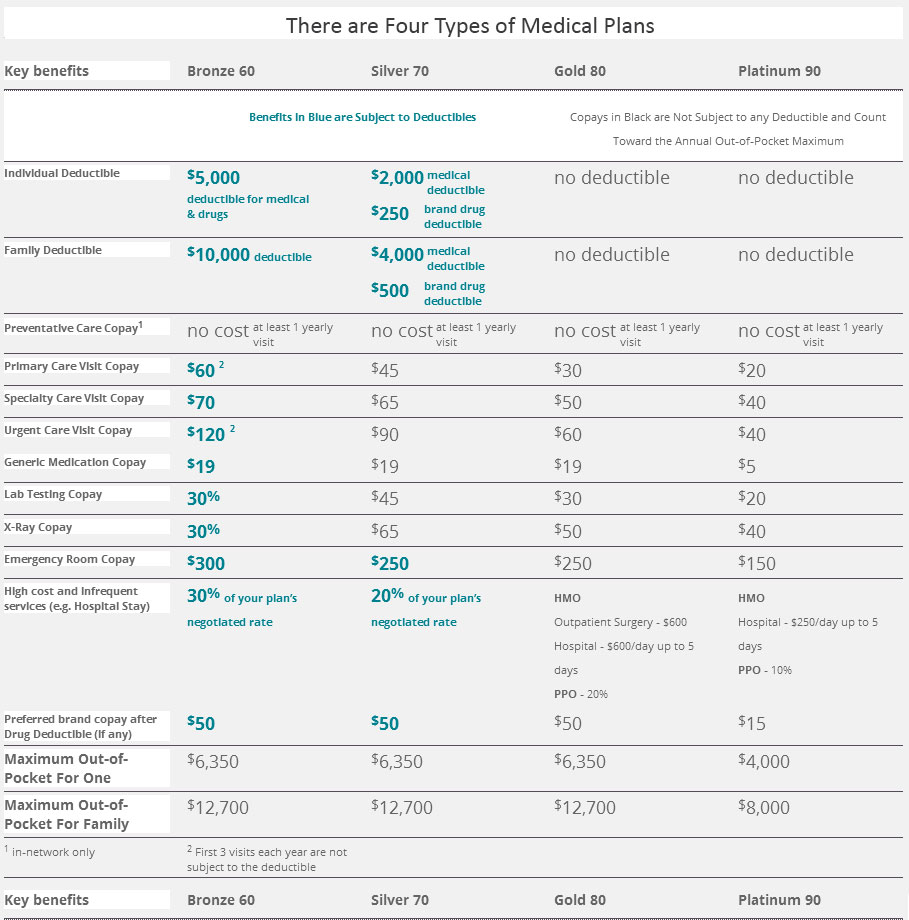

| Key benefits | Bronze 60 | Silver 70 | Gold 80 | Platinum 90 |

|---|---|---|---|---|

| Benefits in Orange are Subject to Deductibles | Copays in Black are Not Subject to any Deductible and Count Toward the Anual Out-Of-Pocket Maximum | |||

| Individual Deductible | $5,000 deductible for medical & drugs |

$2,000 medical deductible $250 brand drug deductible |

no deductible | no deductible |

| Family Deductible | $10,000 deductible | $4,000 medical deductible $500 brand drug deductible |

no deductible | no deductible |

| Preventative Care Copay1 | no cost | no cost | no cost | no cost |

| Primary Care Visit Copay | $60 | $45 | $30 | $20 |

| Specialty Care Visit Copay | $70 | $65 | $50 | $40 |

| Urgent Care Visit Copay | $120 | $90 | $60 | $40 |

| Generic Medication Copay | $15 | $15 | $15 | $5 |

| Lab Testing Copay | 30% | $45 | $30 | $20 |

| X-Ray Copay | 30% | $65 | $50 | $40 |

| Emergency Room Copay | $300 | $250 | $250 | $150 |

| High cost and infrequent services (e.g. Hospital stay) | 30% of your plan's negotiated rate | 20% of your plan's negotiated rate | HMO Outpatient Surgery - $600 Hospital - $600/day up to 5 days PPO - 20% |

HMO - Hospital - $250/day up to 5 days PPO - 10% |

| Preferred brand copay after Drug Deductible (if any) | $50 | $50 | $50 | $15 |

| Maximum Out-Of-Pocket For One | $6,250 | $6,250 | $6,250 | $4,000 |

| Maximum Out-Of-Pocket For Family | $12,500 | $12,500 | $12,500 | $8,000 |

| 1 in-network only | 2 First 3 visits each year are not subject to the deductible | |||

| Key benefits | Bronze 60 | Silver 70 | Gold 80 | Platinum 90 |

Depending on your annual adjusted gross income (line 37 of the 1040, Line 21 of the 1040A, or line 4 of the 1040EZ) you may be qualify for up to two levels of financial assistance. Click here to view the 2015 Income Guidelines. This chart will help you determine which levels of financial assistance you may qualify for.

Level 1: Assistance in lowering your monthly premium. This level applies to all annual incomes listed under the Blue Section of the Income Guidelines chart.

Level 2: Assistance in lowering your monthly premium PLUS Enhanced benefits under the Silver Cost Sharing Reduction plans. Enhanced benefits plans have lowered Deductibles, Copays, and Maximum Out-of-Pocket Costs. This level only applies to annual incomes listed under the Gray section of the Income Guidelines Chart.

There are 3 types of Silver Cost Sharing Reduction plans and the ONLY way to enroll in one of these plans is if your Adjusted Gross Income is listed under Gray Silver Cost Sharing Reductions (CSR) section of the Income Guidelines chart. Click below to view the benefits of the plan you may qualify for and see how it compares to Bronze, Gold & Platinum plans.

Please note that all children under the Age of 19 will qualify for Medi-Cal if your Annual Gross Income is below the 266% on the Income Guidelines chart. This means even if the parents qualify for one of the Enhanced plans listed above, their children under the age of 19 will still only qualify for Medi-Cal. In these cases, parents will be on a separate plan from their children. This is what the Affordable Care Act intended to do for most families that qualify for financial assistance.

If you are you under the age of 30 and you do not qualify for financial assistance according to the Income Guidelines chart, then you may want to consider the Minimum Coverage Plan. This will be the lowest priced plan available for you to purchase. Please keep in mind that premium assistance cannot be used to purchase the Minimum Coverage Plan and it is only available for individuals under the age of 30 unless you qualify for a hardship exception.

Interested in a Health Savings Account (HSA) medical plan? Covered California does offer the Bronze 60 HSA medical plan. Please visit our FAQs to find out why an HSA medical plan might be right for you.

Compare the benefits of all the available Covered California Health Insurance plans by viewing the Covered California benefit comparison chart.

| Plan feature | HMO | EPO | PPO |

|---|---|---|---|

| Designate a primary care physican? | Yes | No | No |

| Need a referral to see a specialist? | Yes | No | No |

| Out-of-network benefit? | No | No | Yes |

| Level of flexibility | Minimal | Medium | High |

| Access to convenience care and urgent care clinics? | Maybe | Maybe | Yes |

Please call contact us via Phone, Text or Email:

Phone: (818) 350-2675

Text: (818) 350-2675

Email: [email protected]

We are Covered California certified, which means we'll help you get health insurance online, via email or over the phone. Our goal is to make acquiring Health Insurance easy for you! We will help you determine if you qualify for financial assistance and make sure you complete the Covered California application correctly. Our services are free, so just have a photo ID, proof of income, and your SSN and we'll take care of the rest!

Individual Deductible This is amount you have to pay before the insurance covers any of the services listed in Blue on the Medical Plans Chart located at top of this page. This is the amount you are essentially self-insuring. You are only subject to the deductible if you need medical attention. Therefore, you only pay for the medical services you get rendered. This amount takes effect on January 1st of every year, so even if you satisfy the deductible in 2014, you will have to meet it again in 2015.

Family Deductible This is amount the entire family combined will have to pay before the insurance covers any of the services listed in Blue on the Medical Plans Chart located at top of this page. The deductible requirement will be waived for all members in the family once two or more people in the family have combined to satisfy this amount. For example, if Mom & Dad both reach their individual deductible amounts ($5,000 each = $10,000 combined) under the Bronze plan, then their children will not have to meet any deductible and will only have to pay the copay amounts listed in Blue on the Medical Plans Chart. Also, if only one person in the family meets their individual deductible, that person will still have satisfied their deductible and the insurance will cover any of the services listed in Blue on the Medical Plans Chart for this person only.

Copay This is the amount you will have to pay the IN-NETWORK Medical provider for that specific service(s) listed on the Medical Plans Chart located at top of this page.

Maximum Out-of-Pocket for One This is the most you will pay for all medical services in a calendar year when using IN-NETWORK Medical providers. This comes into play if you ever need a major medical procedure done. For Example, if you have a baby, you will most likely end up paying this amount to the hospital and doctors when you deliver the baby. This is most you will be responsible for in any calendar year. So even if your IN-Network medical providers charge $100K for a procedure, you will only pay a maximum of $6,350 under the Bronze plan because the insurance company will pay the rest. You will also be 100% covered from that point on. Which means any other medical services you have rendered by IN-NETWORK medical providers will be of no charge to you for the remainder of the calendar year. Having a cap/maximum on your Out-of-Pocket costs is the main advantage to purchasing Health Insurance. Without this cap, your potential Out-of-Pocket costs could be astronomical depending on the medical attention you require.

Maximum Out-of-Pocket for Family This is the most a family will pay for all medical services in a calendar year when using IN-NETWORK Medical providers. Every member in the family will be 100% covered once two or more people in the family have combined to satisfy this amount. For example, if Mom & Dad both reach their individual Maximum Out-of-Pocket amounts ($6,350 each = $12,700 combined) under the Bronze plan, then their children will have also meet their Out-of-Pocket Maximums. Which means all medical services the entire family may have rendered by IN-NETWORK medical providers will be of no charge for the remainder of the calendar year. Also, if only one person in the family meets their individual Out-of-Pocket maximum, that person will still have satisfied their Out-of-pocket maximum and the insurance will cover 100% of any IN-Network medical services for this person only for the remainder of the calendar year.

IN-NETWORK Medical Provider These are doctors and hospitals that have contracted with a specific Health Insurance company. You want to make sure to ALWAYS use IN-Network / Contracted medical providers whenever possible because the cost savings will be substantial. For example, HMO & EPO plans will not even provide coverage if you use an OUT-OF-NETWORK medical provider unless it is a life threatening emergency. PPO plans will offer up to 50% reimbursement of what they would have paid one of their IN-NETWORK medical providers for the OUT-OF-NETWORK services you got rendered, so this reimbursement amount rarely ends up being 50% of what you actually spent. In addition, you will have to manually submit these OUT-OF-NETWORK claims to the insurance company for reimbursement and the processing time is unpredictable. Please visit our Find an IN-NETWORK Provider page to find out which Insurance companies your Doctor is IN- NETWORK / Contracted with.

We can enroll you in Dental & Vision plans over the phone, via email or online.

Phone: (818) 350-2675

Email: [email protected]

Online: Click here to learn more about Dental Coverage - Click here to learn more about Vision Coverage

{kind=link}